A Walk Through The Land of the Rising Sun

A small basket Japanese of net nets

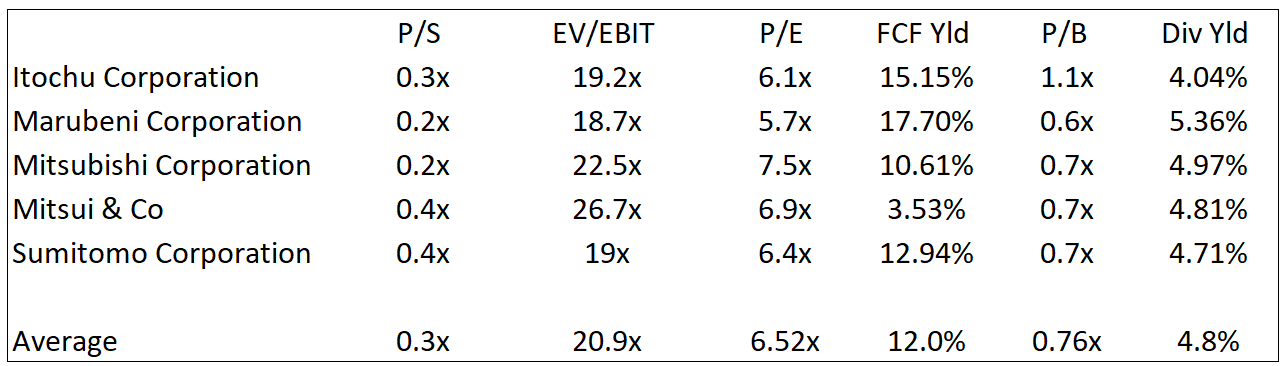

Announced in 2020 Warren Buffett's company Berkshire Hathaway in total invested about $10.6 billion to buy at first 5% stakes in five large Japanese companies: Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo. These companies, known as "sogo shosha," are involved in various businesses like trading goods, managing resources, and investing in different industries. Buffett was attracted to these companies because they were stable, profitable, and paid regular dividends to shareholders. Over time, Berkshire increased its ownership in each company to about 7.4% by 2023. By the end of 2024, the value of these investments had grown to $23.5 billion, showing significant gains. In Berkshire Hathaway 2025 annual report Buffett expressed plans to further increase these stakes in Japan.

Just to give a idea of valuation at the time below I have the company’s he invested in with some valuation multiples. To give context the announcement of his purchase was in 30th August of 2020, assuming it takes 12 months for them to release these documents these numbers are roughly the same numbers Buffett may have been looking at in 30th August 2019. All multiples are in a LTM basis.

I thought it was very interesting that Buffett wants to increase their positions in their Japanese holdings. I thought to myself, ‘‘if Buffett was 20 now what would he buy in Japan’’. After thinking I basically concluded he would buy a basket of net nets. Net nets are investments that Buffetts mentor Benjamin Graham mainly practised. Early in his Buffett’s life he did very well in net nets. Buffett early partnership made a CAGR return of +25.3%. Net nets is the Cash + Accounts Receivable + Inventory - Total Liabilities. If that number exceeds the current market cap you have a investment opportunity. Simply put, NCAV serves as an estimate of a company's liquidation value. If a business were to collect all its receivables, sell off its inventory, settle its all its liabilities, and stop operations, the remaining amount would be available for distribution to shareholders. These tend to work for a couple main reasons. They are simply super cheap. They provide a massive margin of safety and potential for mean reversion as market mispricing’s tend to correct over time.

Criteria

P/NCAV must be below 0.7x

Easy to understand business model

No or low debt

It must have a long track record of profitability

At least 20% of the current assets must be in cash

Honest management with preferably insider ownership

These criteria tend to be ‘‘rules of thumb’’ it’s basically impossible to find all 6 if you find at least 4 out of 6 you have may have a good idea. However, 6 out of 6 criteria is preferable. Below I have a couple quick pitches of some net nets in Japan. For upside I would use P/NCAV of 1.0x. For instance, if a company is trading at a P/NCAV of 0.5x I would consider that a company that has the potential to double.

All information on the financials is from Koyfin and I am only able to see data going back to 2015.

Marufuji Sheet Piling (TYO: 8046)

P/NCAV: Its very cheap at only 0.52x P/NCAV ✅

Business overview: Marufuji Sheet Piling established in 1926 and headquartered in Tokyo, Japan, specializes in the sale, rental, and repair of temporary construction materials, including steel sheet piles, H-shaped steel, and lining boards. They also provide services such as the RG construction method, drive-in/pull-out work, and underground obstacle removal. ✅

Low debt: They have very low debt. Just look at their debt vs cash and book value. ✅

Record of profitability: Since 2015 years Marufuji Sheet Piling has made net income. Their net income has grown at a CAGR of +5.2% since 2015. ✅

Cash: Unfortunately, cash makes up 13% of the current assets and didn’t reach the mark of 20%. ❌

Honest management with preferably insider ownership: There has been no evidence of shareholder dilution which is good. Furthermore 21.33% of the company is held by insiders which is a good sign. ✅

Score: 5/6

Echo Trading Co (TYO: 7427)

P/NCAV: Its cheap at a P/NCAV of 0.55x✅

Business overview: Echo Trading Co is primarily engaged in the pet-related business. Its operations encompass the wholesale of pet food and supplies, provision of pet-related education services, development of pet food, supplies, and pet shops, planning and production of sales promotion tools for pet supplies, and operation of comprehensive pet information websites. Additionally, the company is involved in the wholesale of liquors, food, and related consumer products. ✅

Low debt: They have over double in cash than in debt plus they have a debt to equity ratio of 0.28. ✅

Record of profitability: Their net income has been volatile however they’ve been consistently profitable since 2019. ✅

Cash: Cash makes up 20% of the current assets ✅

Honest management with preferably insider ownership: 42.97% of the company is held by insiders. ✅

Score: 6/6

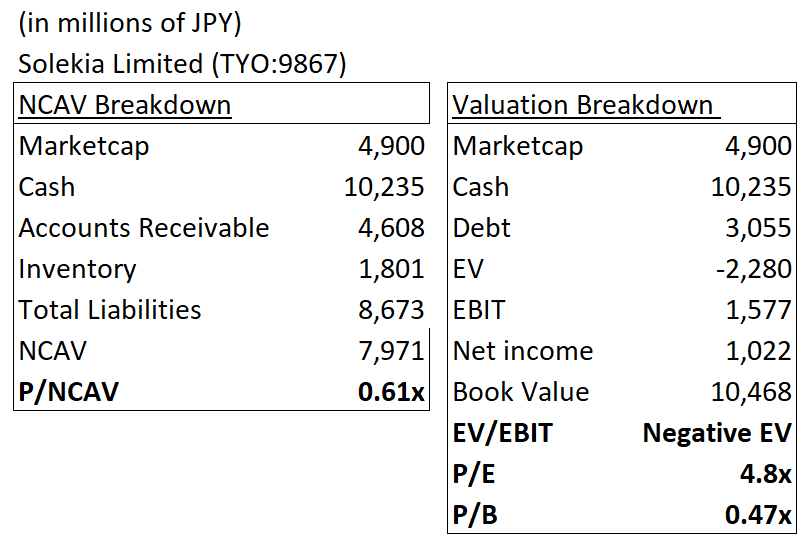

Solekia Limited (TYO:9867)

P/NCAV: Cheap at a P/NCAV of 0.61x ✅

Business overview: Solekia Limited, established in 1958 and headquartered in Tokyo, Japan, is an Information and Communication Technology (ICT) service integrator. The company offers component and device solutions for electronic devices and semiconductors, ICT solutions for system integration, as well as management and field services. Operating through three regional segments—Tokyo, East Japan, and West Japan. Not a very simple business. ❌

Low debt: They have over double in cash than in debt plus they have a debt to equity ratio of 0.29. Plus they have a negative enterprise value which really shows how much cash they have on hand. ✅

Record of profitability: Their net income has been growing very rapidly since 2015. It grew from 189M yen to 1022M Yen LTM. ✅

Cash: Solekia is sitting on a mountain of cash. 61% of their current assets is in cash. ✅

Honest management with preferably insider ownership: 68.82% of the company is held by insiders.✅

Score: 5/6

RKN Finance

I would also like to take some time to share another great substack. RKN Finance, is a platform that provides market news, updates and stock deep dives. I would highly recommend it.

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions. The author may hold positions in the companies mentioned, but the opinions expressed are their own and are subject to change without notice. Investing involves risk, and past performance is not indicative of future results.

Is high insider ownership a good thing, when the company is a net-net? Because high insider ownership leaves little room for activist.