A Tiny Australian Company Trading At 25 Cents On The Dollar

With a 3.6x P/E and 0.25x P/B

Company:Australian Adventure Tourism Group

Ticker:AAT

Exchange: NSX (National Stock Exchange of Australia)

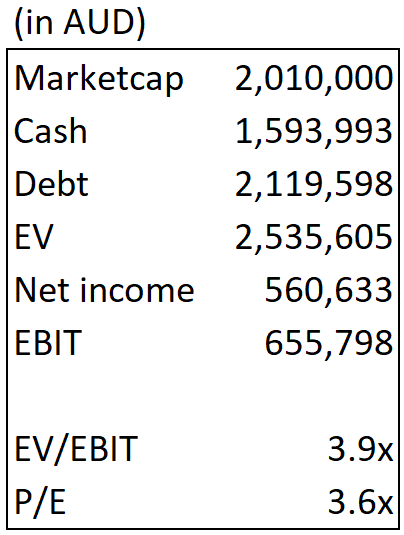

Marketcap: $2,119,598 AUD

Founded: 1984

P/E: 3.6x

EV/EBIT 3.9x

Adjusted book value 0.25x (before was 0.21x)

Company overview

Australian Adventure Tourism (AAT) Group owns and operates Magnums Accommodation, a well-regarded hotel in Airlie Beach. According to the latest annual report, Magnums maintains an occupancy rate 20% above the regional average, highlighting its strong demand. The company also owns and operates the Magnums Tour Office, which provides tour services for visitors. Additionally, the group owns Lot 331, a development property adjacent to Magnums, currently used for parking and access.

Regarding their main business which is the Magnums Accommodation. They are rated very highly on travel websites. For instance on TripAdvisor, they are rated 4 out of 5 with 1070 reviews. On Trivago they are rated 8.1 out of 10 and on Expedia they are rated a 8.2 out of 10. In short their hotel business is a Hotel experience customers in general have enjoyed.

The Numbers and Valuation

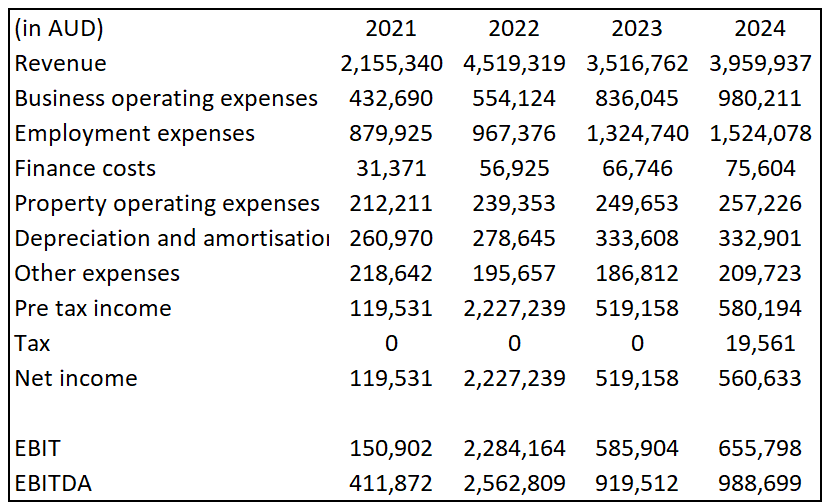

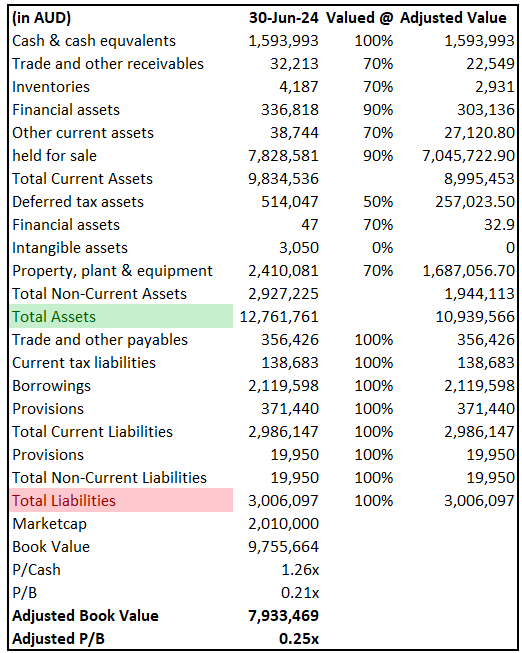

Looking at the quick valuation snapshot its clear its cheap. Trading at a 3.9x EV/EBIT and 3.6x P/E and 79.3% of its market cap in cash. Looking to historical income AAT has performed quite well in recent years. Revenue has been growing at a CAGR of 22.48% with a debt to EBITDA of 2.14x which is pretty manageable. I didn’t include 2020 due to the fact that is obviously was when AAT was heavily impacted by Covid. And I wanted a clearer depiction of earnings. Looking at their balance sheet AAT is very cheap compared to its book value. For instance, without adjustments AAT is trading at 21 cents of the dollar. However, if we do some adjustments and try and get a estimated liquidation value (The value of remaining after selling a company's assets and paying off its debts) we still get a very cheap valuation. At 25 cents on the dollar. A company of this nature should not be trading at 25 cents on the dollar. This is a company with a good hotel business with great reviews online and a 20% above the regional average occupancy rate.

Looking at similar peers I could only find 2 companies that fit. One is Tourism Holdings Limited (THL) which focus on rental and sales of motorhomes and campervans, mainly in New Zealand and Australia. The second is SkyCity Entertainment Group (SKC) another New Zealand company that has Casino and Hotel operations across New Zealand. THL is trading at P/B of 0.6x and SKC is trading at a P/B of 0.8x. Meaning on average AAT peers are trading at 0.7x P/B. If AAT can trade at P/B of 0.7x the marketcap of AAT will be $6.8M AUD. Comparing this with today’s market cap of $2.01M AUD that is a 238% increase.

Looking pass peer valuation and strictly looking at their balance sheet and assume it can trade at my adjusted book value which is my estimated liquidation value of $7.9M AUD we get a increase of 293%.

Cash adjustments to consider: If you scroll up and view the balance sheet. There you will notice they have $336.8K worth of financial assets. Remember this is the most recent financial report release which came out in June. However, on their annual report they state ‘‘The fair value movement in financial assets primarily reflects the movement in the ASX quoted market value of the shares held in Australian Dairy Nutritional Group (ASX Code: AHF). As disclosed in prior years, holding listed investments is not a long-term core activity for the Group. At 30 June 2024, the AHF shares have been classified as current financial assets held for sale and have been subsequently sold on 30 August 2024 for 2 cents’’. Reading their annual report will tell you they owned 15,309,892 shares of Australian Dairy Nutritional meaning the total amount sold was $306,197.84 worth of shares. Because the balance sheet is from June but they sold the shares in August. The extra $306,197.84 is now in cash. Meaning they don’t have $1,593,999 on cash on their balance sheet they actually have $1,900,190.4. However, we will not know for certain until the next financial quarter report comes out.

Whitsunday Skyway Project

Currently AAT is working on another project to add to their existing business model. Its called the Whitsunday Skyway Project. It’s a proposed scenic cable car project and is planned to connect Airlie Beach to Conway National park rising 430 meters above sea level. It would also include mountain bike trails, luge tracks, dining facilities, and Indigenous cultural experiences. Currently the project is is in the Detailed Assessment Phase under the Queensland State Government’s Exclusive Transaction Process. However whats interesting is the Whitsunday Skyway Project received a commitment from the Government, along with $1 million in matched funding for environmental offset land costs. Futhermore AAT has entered negotiations with JV Partner, that is confident that it is likely to be able to introduce a number of other financially capable equity investors to the project. In the future if this project is completed in theory it would bring more income to AAT.

Potential land sale

According to the annual report there is a proposed sale of Magnums Accommodation and the associated properties, Lots 51 and 331. The first part of the sale involves the business sale of Magnums Accommodation, located in Airlie Beach, for $495,000. This amount includes a $300,000 non-refundable deposit and a $195,000 vendor finance agreement. Furthermore, the contract includes a 10-year lease agreement for Lots 51 and 331, at a monthly rate of $98,375, plus outgoings. Furthermore, the contract features call and put options for the future sale of Lots 51 and 331, which are priced at $12,005,000. These options are contingent on shareholder approval. The transaction has faced some uncertainty, as it missed its original settlement date of September 23, 2024, and ongoing negotiations are still in progress. If the transaction goes through, it could provide key benefits for AAT shareholders. The immediate cash inflow from the $300,000 deposit and the potential $12M from the land sale (if the options are exercised) could significantly enhance the company’s liquidity. This capital could be used to reduce existing debt, which stood at $2.1M. Additionally, the proceeds could be used to fund strategic growth initiatives, such as the Whitsunday Skyway Project—a speculative but prioritized venture that could reshape the region’s tourism landscape. The sale may also offer an opportunity to return capital to shareholders through dividends.

Here’s a back of envelope math. Assuming the $12M deal goes through and they only pay out 33% of that $12M back to shareholders they would be paying out $3.9M in dividends. Which is more than the current marketcap. However, this potential land sale is highly speculative since they were supposed to settle this in September of 2024.

Insider Ownership

Insider ownership is very high for AAT which I like 36% of the company is owned by management. High insider ownership aligns the interests of management with shareholders, as insiders benefit directly from the company's success. It can also signal confidence in the business, as insiders are more likely to act in the long-term interest of the company.

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions. The author may hold positions in the companies mentioned, but the opinions expressed are their own and are subject to change without notice. Investing involves risk, and past performance is not indicative of future results.

Looks compelling, are you able to buy shares? Seems like last trade was on March 2024?

Nice write up. I´ve been looking to some of their reports and I have two questions. Maybe you have a thought on them.

1. In 2022 and 2018 they had an item "Other Income" which is not about continuing operations and they have made some impairments on the assets value. I do not think this is very honest but maybe in Australia accounting is right thing to do (does not make sense anyway).

2. Have they invested in more rooms from 2018 to 2024 or they simply got more rooms occupied? There is a difference in revenue of a 100% approx, between those years (2M - 4M). They do not talk about occupancy rate in their annual reports.