A Nick Sleep Type Idea

''Finally a NASDAQ listed idea'' - you

Nick Sleep

Everybody and their mother know who Warren Buffett is. The old billionaire grandfatherly figure who sits in his office in Omaha reading annual reports and eating peanut brittle and drinking Coke. Although he is my favourite investor with Charlie Munger coming in a close second. My third favourite investor is a man who’s known in investor circles but not known to the laymen. His name Nick Sleep.

Nick Sleep is a legend, he started his fund back in 2001 and with his co-worker Zakaria and founded Nomad Partnership. Between starting in 2001 and ending in 2013, Nick and Zak compounded at annualized return of +20.8% per year vs +6.5% for the MSCI World Index. Meaning every $1 put into Nomad Partnership at the start turned into $10.21 by 2013. For instance, $1M turned into $10.21M.

When they shut down their fund in 2013 they only had 3 stocks in their portfolio. Yes only 3. In a nutshell they told their investors ‘’listen, we are going to shut down our fund, but we recommend you buy these 3 stocks. Just put a third interest in each and do nothing’’. These stocks were Amazon, Costco and Berkshire Hathaway. Since 2013 they have outperformed the market massively.

Since 2013 $1M with 1/3 being put into each company as of today is worth a whopping $12.2M. Compared to market, if you put $1M into the S&P 500 back in 2013 it would be worth $5.2M today.

(portfolio 1 being Amazon, Costco, Berkshire Hathaway and portfolio 2 being the S&P 500)

Luckly there is a book (one of my favourites) on Nick and the Nomad Partnership. Its basically the breakdown of the Nomad Partnership annual letters to shareholders. These letters give us a insight into Nicks thinking, for example why did Nick like Costco and Amazon back in 2013. You might be thinking to yourself ‘‘so what? The run is over, Amazon is a $2.4 trillion company its to late for me.’’ Well by learning how Nick thinks about companies we can look at todays companies in the same lens. And I’m going to relate his thinking to a stock I like today which reminds me of Amazon and Costco back in 2013.

Side Note: Learning from history is super important. Not just for investing but for life. For instance, learning about the Tulip mania of the 17th century relates to Bitcoin today. Learning about Dot-com bubble of the early 2000s relates to A.I today. On the topic of learning about life from history let me set the scene. There was once a man who was the greatest musical talent that ever lived. However, he was bitterly unhappy and died young. Who’s this man? Mozart. Mozart did 2 things that guaranteed a lot of misery. Firstly, he overspent his income, and he was full of jealousies and resentment. If a musical genius high IQ man such as Mozart couldn’t be happy from having that behaviour I don’t recommend it for anyone else. Moral of the story? Save your money and don’t be envious and forgive your fellow man for his trespasses.

PDD Holdings

(all in USD)

Stock: PDD Holdings

Ticker: NASDAQ: PDD

Marketcap: $172.43B

P/E (NTM): 10.9x

Business overview

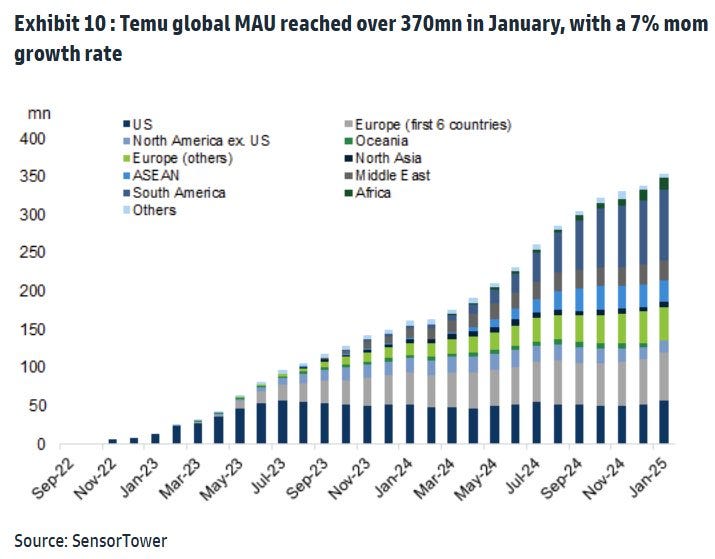

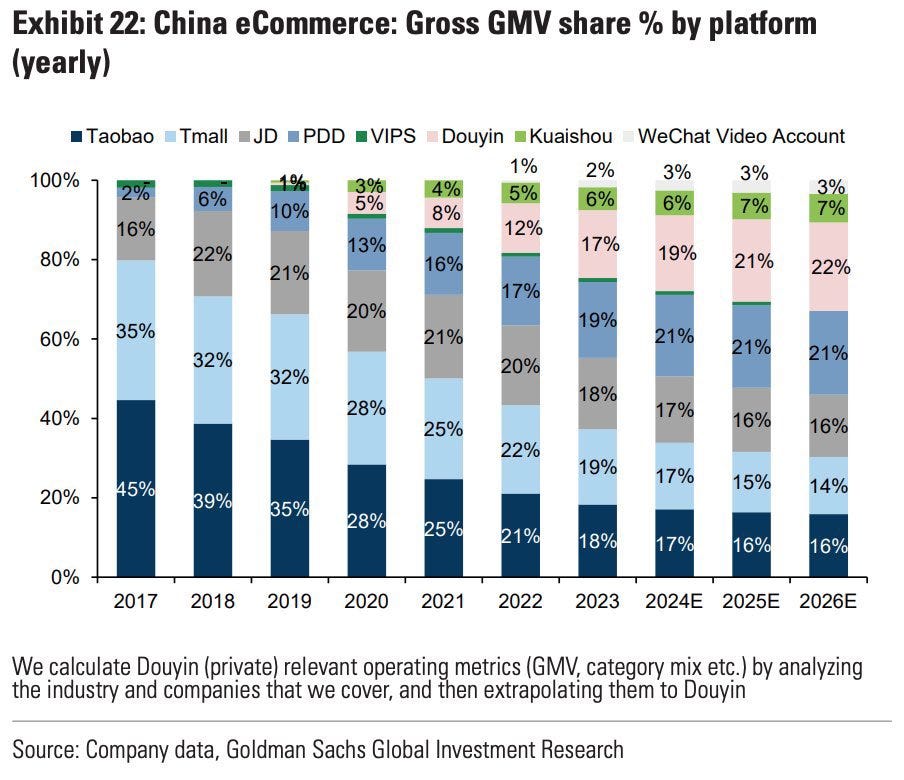

Founded in 2015 as Pinduoduo, the company has grown into China’s second-largest e-commerce player, capturing over 20% market share. PDD’s Consumer-to-Manufacturer (C2M) model, which connects manufacturers directly to consumers eliminated intermediaries, allowing for ultra-low prices that attract price-sensitive consumers and small merchants. Its discovery-based, algorithm-driven shopping experience has created a highly engaging platform, driving user and merchant growth in a virtuous cycle. I expect PDD to continue gaining share in China given its dominance in the value-for-money segment, growing branded product offerings at affordable prices, and high operational efficiency. PDD’s network effects and cost advantage, supported by its lean structure and efficient C2M model, are set to grow as it scales, both domestically and internationally. Its cross-border e-commerce platform, Temu, launched in September 2022, has rapidly become one of the world’s fastest-growing apps. Leveraging China’s excess capacity and PDD’s supply-chain efficiency, Temu wields strong pricing power over Chinese suppliers and attracts overseas consumers with competitively priced products.

PDD has been growing very rapidly. Regarding Gross Merchandise Value (GMV) which refers to the total value of merchandise sold over a specific period of time through a company's platform or marketplace. They’ve increased their market share from 2% in 2017 to 19% in 2023.

Financials

The financial are absolutely mind blowing. PDD has extremely great historical growth with exceptional return on invested capital with almost no debt. I love businesses like this. This is akin to being a basketball coach and seeing a 6’5 15-year-old. I drew a line to separate FY20 and FY21 to separate when ‘’normal’’ earnings started.

Compound annual growth rates since 2021

Total Revenues = 53%

Gross Profit = 50%

Operating Income =140%

Net Income = 133%

Total Equity = 50%

Valuation and peers

Marketcap: $172.43B

Ultimately PDD is a cheap company. A company with an increasing market share, high return on invested capital, and high earnings growth all trading at a P/E (NTM) of 10.9x. In the past PDD has delivered high net income growth with recent high ROIC. Assuming PDD can grow net income at 10% till 2029. We get an estimated net income of $24.8B. Assuming it can trade at a conservative P/E of 10x we get a market cap of $248B. With a current market cap of $172B.

Nick Sleep Letter Quotes

‘‘ What characteristics could one bestow on company that would make it the most valuable in the world ? What would it look like? Such a firm would have a huge marketplace (offering size), high barriers to entry (offering longevity) and very low levels of capital employed (offering free cash flow)’’ - Nomad Partnership 2004 Letter

Let’s apply this quote from Nick Sleep 2004 Letter to PDD. Do they have a large marketplace? They have been growing rapidly in China and with Temu they are now global. In short there marketplace is counted in the billions. Thats a tick✅

Do they have high barriers to entry? Looking at their property plant and equipment PDD has $811.6M on their balance sheet. It would take at least $100M for a new competitor to even try to compete with PDD. That’s another tick. ✅

Do they have low levels of capital employed? I would say so, they have next to no debt compared to their equity and have a high return on invested capital. Their ROIC for the LTM is 31%. ✅

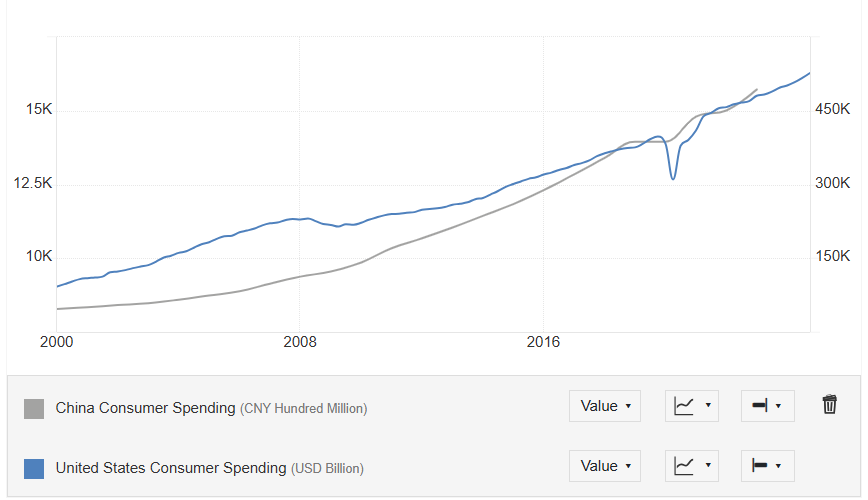

‘‘To those who argue Amazon is large already we ask two questions: what do you think e-commerce will be as a proportion of US retailing in ten-years’ time, and what do you think it was last year?’’ Nomad Partnership 2007 Letter

In regards to the quote above I have the chart below to answer the questions. In short, I think as consumer spending increases overtime PDD has a lot of growth potential. Even though they are already a large company at a market cap of $172B. Looking at Amazon for example, their revenue in 2015 was $107B now its $637B. There will be ups and downs in regards to consumer spending but I think over a 3-5 year time frame consumer spending tends to increase ( I’m not a economist). ✅

‘‘In the office we have a white board on which we have listed the (very few) investment models that work and that we can understand. Costco is the best example we can find of one of them: scale efficiencies shared. Most companies pursue scale efficiencies, but few share them. It’s the sharing that makes the model so powerful. But in the center of the model is a paradox: the company grows through giving more back.’’ - Nomad Partnership 2004

To answer this question, we must first understand what Nick means when he says ‘’ scale efficiencies shared’’. Scale Economies Shared is a concept that Nick Sleep and Qais Zakaria, former fund managers of Nomad Investment Partnership, used to describe a business model where companies pass on cost savings from scale to customers instead of maximizing short-term profits. This creates a reinforcing competitive advantage over time. For instance, Costco runs at razor thin margins (~2-3%) but continuously lowers prices for customers, reinforcing its dominance.

PDD exhibits scale efficiencies shared by aggregating consumer demand through group buying, enabling suppliers to sell in bulk and reduce costs, which are passed on to consumers through lower prices. It also cuts out middlemen, directly connecting manufacturers and farmers to customers, further lowering costs and reinforcing engagement. ✅

Risks

PDD carries some serious risks. The company is highly secretive—employees are banned from interviews, advertising, and even listing bios on job sites, which is a red flag. However, its financials are audited by EY, a top accounting firm, so I’m not too concerned about reporting risk. I could dive into economic and geopolitical risks, but I generally avoid those. Yes, China’s economy is struggling, but long term, I think it will be fine (though I’m not an economist). You might be thinking to yourself ‘’why not write about geopolitical or economic risk’’. Well in the Berkshire Hathaway’s 2018 Shareholder Letter Buffett wrote ‘‘In the 54 years we (Charlie Munger) have worked together, we have never forgone an attractive purchase due to the macro or political environment, or the views of others’’

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions. The author may hold positions in the companies mentioned, but the opinions expressed are their own and are subject to change without notice. Investing involves risk, and past performance is not indicative of future results.

I love your work, man! When considering the economies of scale shared model, do any other companies come to mind?

I linked to your post in my Monday EM links collection post: https://emergingmarketskeptic.substack.com/p/emerging-markets-week-february-17-2025 plus had written about my experiences ordering from Temu/Shopee/Lazada/Amazon: https://emergingmarketskeptic.substack.com/p/can-temu-take-on-amazon-and-the-rest-of-world

Frankly, eCommerce platforms are practically commodities now BUT I strongly try to avoid giving Jeff Bezos more $ - I noted in another post:

"Interestingly enough, Tucker Carlson just interviewed an Amazon seller https://twitter.com/TuckerCarlson/status/1789052798870471092 who appeared in a recent documentary (Amazon — Market. Power! Monopoly? | How Amazon Hikes Prices & Copies Product https://youtu.be/8L6MaNVNBuQ ) and sells a $17 product - of which, Amazon takes $10 leaving him with just $7 to cover the product’s cost, rent, employees, etc. And if he tries to sell his product cheaper elsewhere, Amazon’s computers will detect it and he looses his Amazon “buy box” along with most of his sales."

I've ordered all kinds of stuff from Temu when visiting the states - 4 garden trellises, security cameras, etc... My dad has ordered a food dehydrator, battery operated pruning shears etc... Usually pretty good deals - you just have to wait up to a week+ if in California... Not so sure I'd want to own the stock though as like I said, eCommerce is almost a commodity!